Copyright © 2022 Global Sky Business. All Rights Reserved.

Brazil is the World's Largest Soybean Producer

Soybean is the largest crop in Brazil and the grain continues to be of great importance in the economic trade balance, being a powerful engine that encourages exports and expands the frontiers of Brazilian agribusiness worldwide.

Campaign Status 2021/22

For the 2021/22 campaign, soybean production is forecast at 122.43 million tons, a reduction of 11.4% compared to the previous harvest (138.15 million tons). The good rainfall that occurred in practically the entire country helped in the recovery of a small portion of crops sown late in the South Region and in Mato Grosso do Sul, but did not reverse the decline in productivity, already announced in previous surveys.

Rio Grande do Sul remains the state most affected by the water deficit in November and December 2021, followed by Paraná and Mato Grosso do Sul. In the opposite scenario, most of the other states achieved higher yields than those obtained in the last harvest, with emphasis on Piauí, which has obtained 12.7% higher yields so far. Mato Grosso, Mato Grosso do Sul and Goiás are approaching the end of the harvest, surpassing more than 97% of the sown area.

Estimates indicate an average productivity of 3,000 kg/ha and a total production of 122.43 million tons, down 14.9% and 11.4%, respectively. The drop in production was not greater only due to the 4.1% increase in the sown area, reaching 40,804.9 million hectares in this harvest.

For the 2021/22 harvest, there was a reduction in the estimated exports of 3.16 million tons, from 80.16 million tons to 77 million tons.

There was an increase in crushing of 3.57 million tons from 42.93 million tons to 46.50 million tons.

The reduction in export estimates and the increase in domestic crushing are motivated by an expectation of lower soybean exports in the second half of the year, given that, with crushing margins very attractive, crushing and soybean oil exports should be high and, therefore, soy oil exports are now estimated at 1.56 million tons.

As a result of the increase in the estimate of soybean crushing in grains and the reduction in the estimate of exports, the carryover stocks of soybeans in grains are estimated at 2.52 million tons by the end of 2022.

Evolution of World Soybean Production

The 3 Countries that Produce more than 80% of the World's Soybean

Evolution of Brazilian Soybean Production

[2021/22]

Campaign

[40,804 millions ha]

planted area

[3.000/ha]

Forecast Yield

[122,43 millions Tons]

Forecast Production

South America will produce more than half of the world's soybeans for the tenth consecutive campaign

Uneven evolution: in the last 20 cycles, Brazil doubled its soybean harvest, Paraguay doubled it and Argentina only increased it by 50%. In contrast to the regional trend, our country contracted the area devoted to oilseeds.

The 2021/22 campaign will once again have four South American countries among the 10 largest soybean producers in the world. The combined harvests of the southern cone will represent 55% of global soybean production, maintaining the share achieved last season.

Two decades ago, South American production contributed 48% of the world’s beans, with a supply that was strongly concentrated in the United States (38% of world production). South America exceeded 50% participation in the 2007/08 campaign, when the relative weight of the United States fell to 33%. South American soybeans achieved the largest share of world supply during the 2019/20 cycle, contributing 57% of production. At that time, the result of the United States had decreased due to less planted area and lower yields.

World Soybean Production 2021-2022 - South America Vs Rest of the World

In the last 20 campaigns, world soybean production has increased by 95%. The volume harvested went from 197 Mt in 2002/03 to an estimated 384 Mt in 2021/22, almost doubling. Beyond this strong increase in global production, South American soybean harvests showed an even more spectacular growth in the same period. Regional production went from 93.9 Mt in 2002/03 to an estimated 212.3 Mt in 2021/22, exhibiting a growth of 126% and more than doubling. In 2021/22, the southern cone would exceed the 200 Mt production barrier for the first time. According to USDA data, Brazil is expected to consolidate a harvest of 144 Mt, equivalent to the total South American production a few years ago, in the campaign 2012/13.

Next, trends in soybean area, yield and production will be analyzed for the main originating countries of the oilseed in South America: Brazil, Argentina, Paraguay, Uruguay and Bolivia.

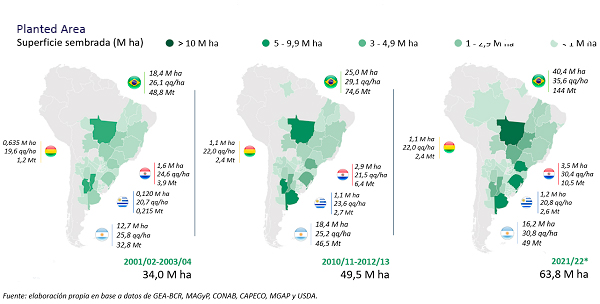

At the beginning of the century, the area devoted to soybean cultivation in the region accumulated 34.0 M ha, an area equivalent to the entire territory of Germany. In the average of the 2001/02-2003/04 campaigns, Brazil planted 54% of the area of South America, Argentina 37% and Paraguay 5%. Ten campaigns later, in the southern cone, close to 50 M ha were already covered with soybeans, and all the countries analyzed had a total area sown with the oilseed.

Currently, it is estimated that South American farmers will complete their planting on 63.8 M ha in the 2021/22 cycle. The target area is equal to the entire territory of France. In the next campaign, Brazil will plant 63% of the area planted in South America, Argentina 25% and Paraguay 5%.

The evolution of the participation in the regional sowing of each country reveals the different tendencies observed in each one. Brazil, which has always been the leading regional producer, more than doubled the area dedicated to soybeans in the last 20 years (+120%). The growth in the area was sustained thanks to the increase in the planted area in areas where soybeans were usually grown, such as the Center-West Region (Mato Grosso, Goiás, Mato Grosso do Sul), the South Region (Rio Grande do Sul, Paraná, Santa Catarina) and the Southeast Region (Minas Gerais, Sao Paulo). Mato Grosso, the main producing state, went from producing 3.1 Mt in 2002/03 to 10.3 Mt in 2021/22. In turn, the larger area was also achieved thanks to the incorporation of new productive lands for oilseed cultivation. In recent decades, the Brazilian production frontier has expanded considerably, particularly towards the Northeast (Bahía, Maranhao, Piauí) and North (Tocantins, Pará, Rondônia) regions. The growth of the area devoted to oilseeds allowed Brazil to increase its participation by almost 10 percentage points, going from a share of 54% at the beginning of the period to 63% today.

The planted area in Paraguay grew in a proportion similar to that of Brazil, 119%. The greatest increase in the area occurred in the departments of the territorial east, mainly in Canindeyú, Caaguazú, Alto Paraná, San Pedro and Itapúa.

Argentina also increased the area dedicated to soybeans, although in a much smaller proportion. The area sown in 2021/22 is expected to be just 28% above that cultivated 20 seasons ago. In the case of Argentina, the area devoted to oilseeds has been shrinking in the last 6 cycles, and the trend is expected to continue in 2021/22 as well. The lower participation of soybeans in the Argentine production plan is explained, on the one hand, by the competitiveness gained by corn and the combinations that this grain offers depending on the area. On the other hand, the high rates paid by soybeans and their industrial derivatives as export duties limit the price that can be paid for the oilseed in the domestic market. Consequently, there are smaller margins for soy plantations in many regions that today choose to intensify the cultivation of corn and wheat, mainly.

Soybean Production in South America

The best average yields in the region are found in Brazil. For the 2021/22 campaign, a yield of 35.6 qq/ha is expected for the Brazilian oilseed, 9.5 qq/ha more than what was obtained at the beginning of the millennium. The average yield in Argentina is anticipated at 30.8 qq/ha, consolidating itself as the second best in the region. Although there is evidence of an improvement of 5 qq/ha in the last 20 campaigns, this is practically half of the increase in Brazilian unitary productivity. In the case of Paraguay, it is expected that, on average, it will obtain 30.4 qq/ha in the cycle, 5.8 qq/ha above the records at the beginning of the 2000s. Finally, Bolivia and Uruguay exhibit higher yields modest, which have also grown to a lesser extent during the last decade.

Having already analyzed the evolution in the planted area of each country and the yields obtained in each region, it is not surprising that in terms of production, Brazil continues to be the undisputed leader. From each to the 2021/22 cycle, the South American giant would harvest 144 Mt -almost 3 times its average harvest 2002/02-2003/04-, Argentina 49 Mt -50% more-, Paraguay 10.5 Mt -more than doubling production-, Uruguay 2.6 -about 12 times more- and Bolivia 2.4 Mt -doubling the harvest in 20 years-.

We offer a complete range of commodities originating in South America.

Contacts

- Brazil: Av. Santos Dumont N°1883, Floor 5th, office 532/533, Aero Empresarial Building, Lauro de Freitas, Bahia, Brazil.

- Argentine: Tucuman 1946, Office N°04 - Córdoba, Argentina.

- info@globalskybusiness.com

- +55 71 98205 1492

Main Commodities

Subscribe

Follow our newsletter to stay updated about agency.