![]()

POWDER MILK

Size and market share of powdered milk

The powdered milk market is expected to grow from $35.11 million in 2025 to $36.45 million in 2026 and is projected to reach $43.95 million in 2031, with a compound annual growth rate (CAGR) of 3.81% between 2026 and 2031. Powdered milk, a dehydrated form of liquid milk, is widely used in various industries, including infant formula, confectionery, bakery products, beverages, and nutritional supplements. Its long shelf life, ease of storage, and transportation advantages make it a preferred choice for both manufacturers and consumers. Market growth is primarily driven by increasing demand for convenient and long-lasting dairy products, especially in regions with limited access to fresh milk. Growing health awareness among consumers has further boosted demand for powdered milk, particularly for fortified and organic varieties that meet specific dietary needs. The growing adoption of powdered milk in emerging economies, where it serves as a cost-effective alternative to liquid milk, is another important factor contributing to market expansion. Furthermore, the food and beverage industry is increasingly incorporating powdered milk into its products to enhance nutritional value and improve product stability.

Key findings of the report

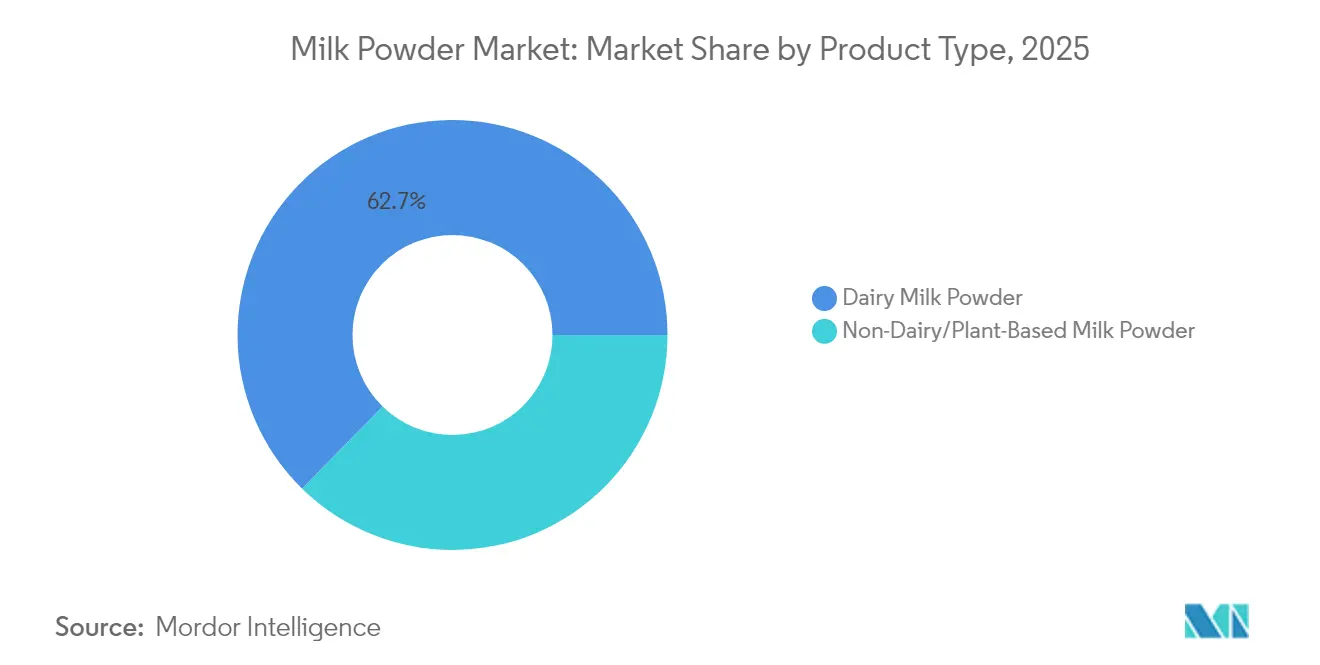

• By product type, powdered milk accounted for 62.68% of the powdered milk market share in 2025; non-dairy alternatives are projected to have the fastest CAGR at 3.92% through 2031.

• By distribution channel, retail controlled 55.72% of the powdered milk market share in 2025, while foodservice is projected to expand at a CAGR of 4.85% through 2031.

• By packaging, flexible pouches led with a 37.58% revenue share in 2025; single-serve sachets are projected to grow at a CAGR of 4.60%.

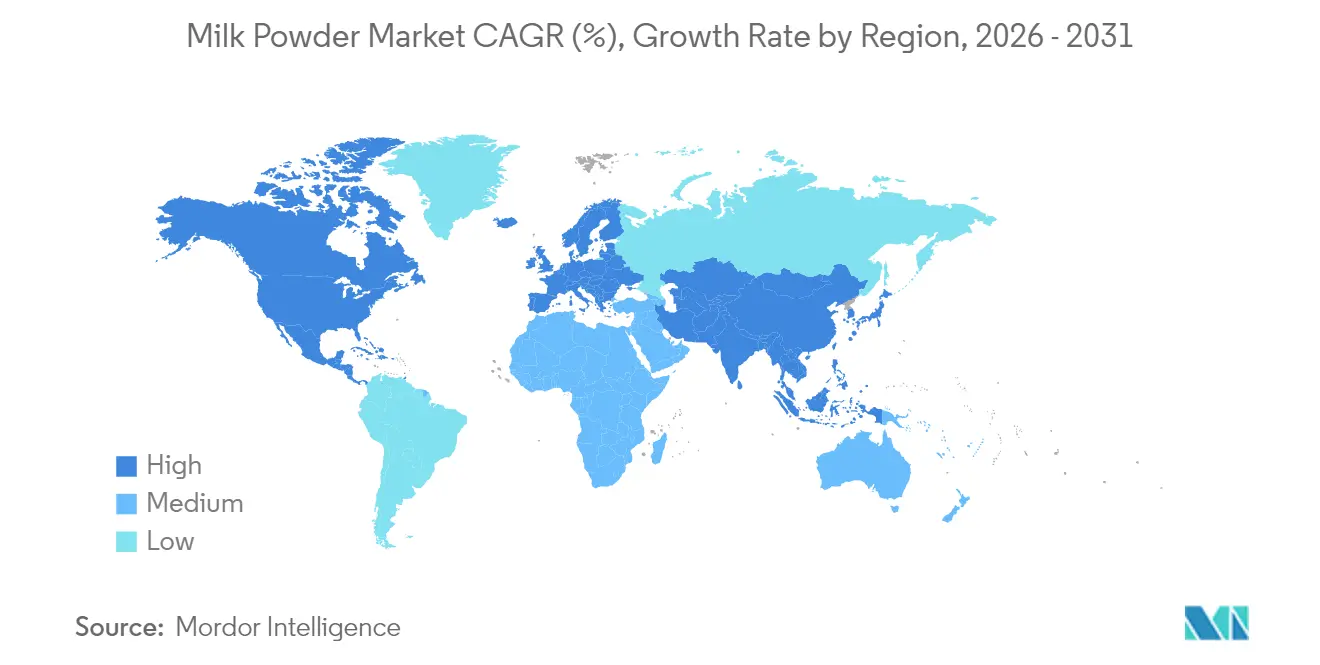

• By geography, Asia-Pacific contributed 41.62% of 2025 revenues, while the Middle East and Africa are projected to advance at a compound annual growth rate of 4.90% through 2031.

Segment analysis

By product type: Powder milk predominates, but plant-based alternatives are gaining ground.

In 2025, powdered milk dominated the market, holding a 62.68% market share. This dominance is due to its widespread use in various applications, such as infant formula, bakery products, confectionery, and beverages. Its long shelf life, ease of transport, and nutritional benefits make it the preferred choice for both consumers and manufacturers. Furthermore, this segment benefits from the growing demand for high-protein diets and the increasing consumption of ready-to-eat and processed foods. Emerging markets, particularly those in Asia-Pacific, are experiencing a surge in demand for powdered milk due to rising disposable income and changing dietary habits. Advances in processing technologies and the availability of fortified powdered milk are also expected to sustain the segment’s growth throughout the forecast period.

On the other hand, non-dairy alternatives, such as plant-based milk powders, are experiencing rapid growth, with a projected compound annual growth rate (CAGR) of 3.92% through 2031. This growth is driven by increasing consumer preference for vegan and lactose-free products, along with greater awareness of environmental sustainability. Plant-based milk powders, derived from sources such as soy, almond, and oat, are gaining traction due to their health benefits and suitability for people with dietary restrictions. The segment’s expansion is further fueled by product innovation, such as flavored and fortified varieties, which cater to diverse consumer preferences. In addition, the growing adoption of plant-based diets, supported by marketing campaigns and the endorsement of health and wellness influencers, is driving demand. The increasing availability of plant-based milk powders in major retail channels and their integration into various food and beverage applications are expected to further fuel growth in this segment.

Geographic analysis Source:

By 2025, the Asia-Pacific region is projected to secure a dominant 41.62% market share in the powdered milk market, driven by several key factors. The region’s expanding population, coupled with rising disposable income, has significantly increased consumer purchasing power, facilitating greater access to packaged dairy products, including powdered milk. Urbanization trends are further intensifying this demand, as urban consumers increasingly prefer convenient, long-life dairy options. Furthermore, China’s regulatory landscape is undergoing significant changes, with the introduction of new national food safety standards and restrictions on the use of powdered milk in long-life milk. While these regulations may cause short-term disruptions, they are also raising quality standards, benefiting producers who meet these stringent requirements and positioning them for long-term growth in the market.

The Middle East and Africa region is experiencing the fastest growth in the milk powder market, with a projected compound annual growth rate (CAGR) of 4.90% through 2031. This rapid growth is supported by continued economic development and substantial infrastructure improvements, which are crucial for the efficient distribution and consumption of dairy products. As disposable incomes rise and urbanization progresses, demand for milk powder and other dairy products is expected to grow steadily. Furthermore, government initiatives aimed at improving food security and promoting local dairy production are likely to drive market expansion in this region, creating opportunities for both domestic and international players.

North America and Europe exhibit stable growth patterns, reflecting the maturity of their respective milk powder markets. These regions benefit from consolidated supply chains, high consumer awareness, and consistent demand for dairy products. However, growth opportunities remain limited compared to emerging markets. In contrast, South America presents a promising outlook for the powdered milk market, driven by economic development and the growth of the middle class. As consumers in this region increasingly seek nutritionally enhanced products, a rise in demand for powdered milk is anticipated. Furthermore, the region’s growing focus on improving dairy production capacity and expanding export opportunities is further fueling market growth.

Argentine Powder Milk

Argentina is a significant producer and exporter of powdered milk worldwide, ranking fifth in whole milk powder production in 2021. With a strong export focus (especially to Algeria, Brazil, and Russia), the country has highly automated plants, mainly located in Santa Fe, Córdoba, and Buenos Aires.

Key aspects of powdered milk production in Argentina:

Productive Leadership: Argentina is one of the world’s leading players, frequently ranking among the top 10 producers and exporters of powdered milk, with whole milk being the most processed variety.

Exports: The main export destinations are Algeria (accounting for over 60% of sales during certain periods), followed by Brazil, Russia, and China.

Main Companies: Mastellone Hnos. (La Serenísima), Saputo, Nestlé, Williner (iLoLay), CORLASA, and Lácteos La Ramada, among others, stand out for their drying and processing capacity.

Process and Quality: Production is characterized by a high level of automation, converting raw milk with high water content into powder with approximately 3% moisture, meeting international standards.

Production Regions: 90% of dairy production is concentrated in the provinces of Santa Fe, Córdoba, and Buenos Aires. The Argentine dairy industry, including the production of powder milk, is an important pillar of the national agribusiness, with sustained growth in export capacity over the last decade.

Powder milk was Argentina’s leading dairy export in the first five months of 2025, accounting for 40% of the sector’s total exports. It’s worth noting that powdered milk’s share has declined over the years, having reached 70% of the total at the beginning of the century, and has lost ground to cheese and whey exports. Thus, from January to May of this year, exports of these two products represented 28% and 23%, respectively, of the sector’s total export volume.

Regarding the destination of exports, it is noteworthy that the dairy export market remained concentrated: in the first five months of the year, 70% of shipments abroad went to just four countries. In fact, the main trading partner for the dairy sector was Brazil, which received 42% of Argentine dairy exports. Algeria followed, with 12% of shipments, while China and Chile accounted for 10% and 6% of exports, respectively. It should be noted, however, that a considerable portion (27%) of the destinations of Argentine dairy exports are unknown due to the application of statistical secrecy regulations by INDEC (National Institute of Statistics and Censuses).

Prices and international outlook.

Given the decline in dairy export volume during the first five months of the year, the increase in the value of shipments is explained by a rise in product prices. According to data published by the Secretariat of Agriculture, Livestock and Fisheries (SAGyP), the export price of whole milk powder has been rising over the last year and a half, accumulating a 32% increase since November 2023. Thus, the FOB price of this product in May 2025 is estimated at US$4,185/ton, well above the historical average of US$3,570.

Availability:

Immediate

Product Origin:

Argentina

Delivery term:

15 days

Buyer’s Documents:

LOI & RWA

Incoterms:

FOB / / CFR / CIF

Payment Terms:

30% Advanced TT. 70% Remaining, L/C against Shipping Documents

Avaikability:

Immediate

Incoterms:

FOB / CIF

Buyer’s Doc.:

LOI / RWA

Delivery Term

45 days

Product Origin:

Brazil / Colombia

Payment Terms:

30% Advanced TT. 70% Remaining, L/C against Shipping Documents

Twitter

Facebook-f

Linkedin-in

Instagram

![]()

We offer a complete range of commodities originating in South America.

Facebook-f

Twitter

Linkedin-in

Instagram

Contacts

Brazil: Av. Santos Dumont N°1883, Floor 5th, office 532/533, Aero Empresarial Building, Lauro de Freitas, Bahia, Brazil.

Argentine: Tucuman 1946, Office N°04 – Córdoba, Argentina.

info@globalskybusiness.com

+55 71 98205 1492

Main Commodities

- Soybean

- Yellow Corn

Svg Vector Icons : http://www.onlinewebfonts.com/icon

Sugar

Beef

Svg Vector Icons : http://www.onlinewebfonts.com/icon

Chicken

Subscribe

Follow our newsletter to stay updated about agency.

Copyright © 2022 Global Sky Business. All Rights Reserved.